Property management firms that screen well share one trait: their criteria are built on documented risk analysis rather than individual discretion. HUD reinforced this principle in its April 2024 guidance on tenant screening, establishing that providers should screen applicants only for information relevant to the likelihood that they will comply with their tenancy obligations. The federal framework is clear. The gap is in how firms translate that standard into daily operations.

I spent 17 years in property management. Leasing agent, property manager, sales, interim COO of a Midwest firm, Regional VP of a California-based company. Along the way, I wrote and rewrote tenant selection criteria for portfolios of different sizes and asset types. The principle that held true throughout was simple: the strongest screening policies are the ones where each criterion can be explained in terms of the specific risk it addresses.

Risk Analysis as the Foundation

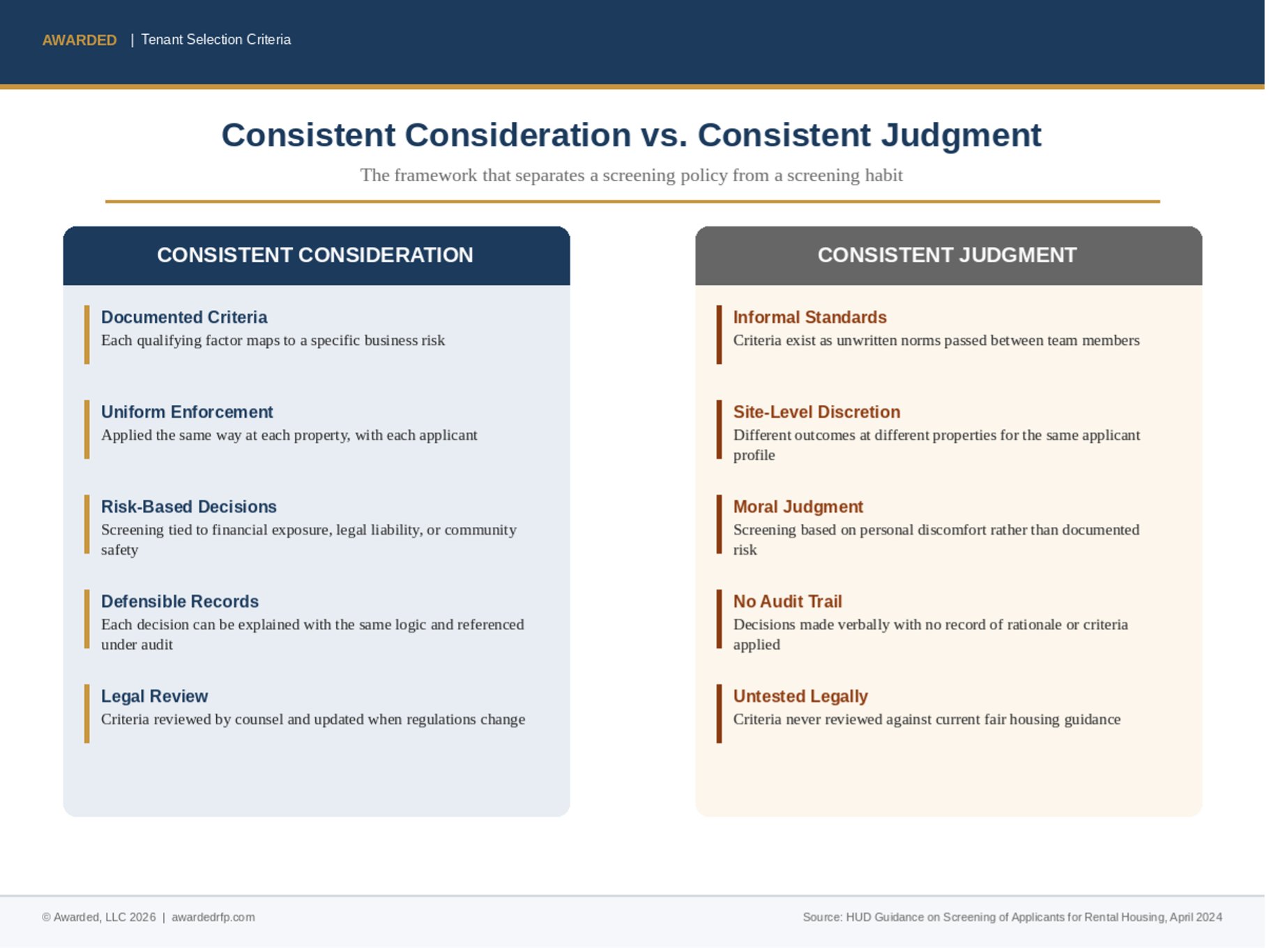

The most effective tenant selection criteria share a common structure. Each qualifying factor maps to a specific business outcome. Fraud and theft on an applicant’s record correlate directly with delinquency risk and the likelihood of financial loss to the owner. Drug-related history may signal that an applicant will attract activity into the building that compromises the safety and stability of the broader community. Certain offenses warrant automatic disqualification regardless of context.

Outside of those clear cases, the question that should guide each criterion is straightforward: what does this behavior predict about the applicant’s tenancy, and can the standard be applied identically each time?

This is what I call “consistent consideration” as opposed to “consistent judgment.” Consistent consideration means all applicants are measured against the same documented criteria, and all decisions can be explained with the same logic. The standard holds across properties, across team members, and across time. When firms achieve that level of uniformity, their screening process becomes an institutional asset rather than a collection of individual preferences.

The Value of Uniform Enforcement

Written criteria only protect the firm when they are applied the same way at each property, with each applicant, on each occasion. A screening policy that allows room for informal interpretation at the site level introduces variability that is difficult to track and harder to defend.

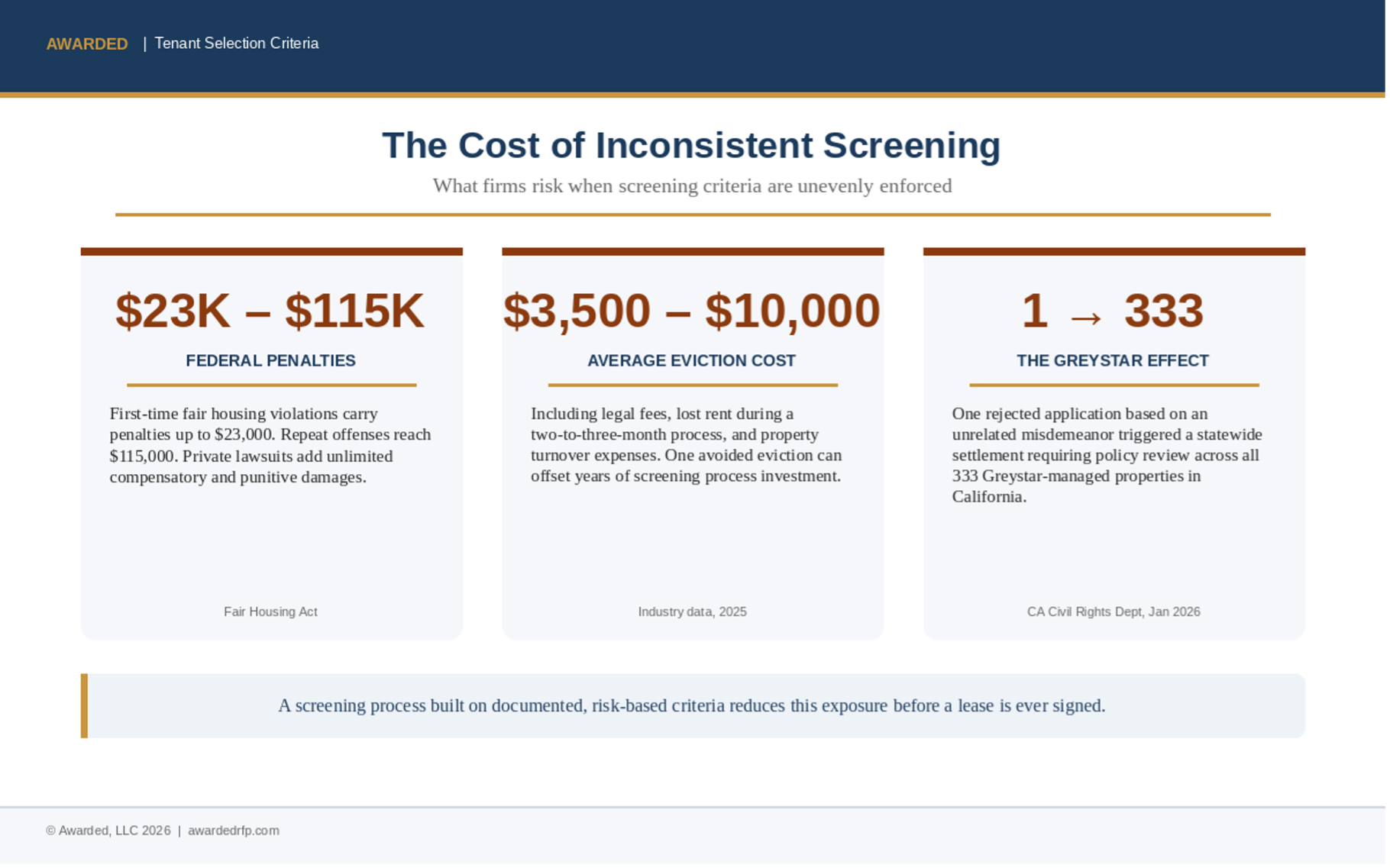

The consequences of inconsistency are not theoretical. Federal fair housing penalties reach $23,000 for first-time violations and up to $115,000 for repeat offenses, with private lawsuits carrying unlimited damages including compensatory awards, punitive damages, and attorney fees. In January 2026, the California Civil Rights Department reached a settlement with Greystar, which manages approximately 333 apartment complexes across the state, after a single prospective tenant’s application was rejected based on an unrelated misdemeanor. The settlement required the company to review and revise its tenant screening policies statewide. One application, handled inconsistently, triggered a policy overhaul across an entire portfolio.

The distinction between market-rate and regulated housing matters here as well. In public housing and tax credit properties, the regulatory framework defines much of the screening boundary. In market-rate environments, firms have greater latitude in setting their own thresholds. Regardless of asset type, the principle remains the same: criteria that are written, legally reviewed, and uniformly enforced carry less institutional risk than criteria that exist informally.

Where Credit and Background Diverge

One of the most practical distinctions in tenant screening is between financial history and behavioral history. Credit challenges are often addressable. A co-signer, a larger deposit where permitted, or a payment plan for outstanding balances can bring an otherwise qualified applicant into compliance. Credit is a solvable variable, and firms that build flexibility into this part of their criteria expand their applicant pool without increasing exposure.

An unfavorable background finding operates differently. The criteria exist to protect the community, the property, and the owner, and the room for accommodation is narrow by design. Firms that maintain a clear, written framework for individualized assessments, including who has authority to review findings and what factors are weighed, preserve both rigor and fairness without relying on ad hoc decision-making.

The financial case for getting this right at the front door is straightforward. The average eviction costs property managers between $3,500 and $10,000 when factoring in legal fees, lost rent during a typical two-to-three-month process, and property turnover expenses. A screening process built on documented, risk-based criteria reduces that exposure before a lease is ever signed.

Technology as Infrastructure, Not Strategy

The screening platforms available today deliver clean, fast, reliable data. Products like Amrent and Boom give operators access to criminal records, credit history, rental verification, and identity authentication in formats that are immediately usable. The technology side of tenant identification has matured significantly over the past decade.

Where firms gain the most advantage is in what happens after the data arrives. A screening platform can surface a finding. The value is created by the written policy that defines how that finding is evaluated, by the training that ensures team members apply the same standard, and by the documentation that records the outcome. The platform is infrastructure. The competitive advantage lives in the process wrapped around it.

Building Criteria That Hold

Firms that invest in building rigorous, well-documented screening criteria position themselves favorably in several dimensions. Operationally, consistent standards reduce the time spent on exceptions and escalations. Legally, uniform enforcement creates a defensible record. Competitively, firms responding to RFPs or pursuing new management contracts can present their screening process as a structured, auditable system rather than a general capability.

Three practices anchor that effort. First, each criterion in the tenant selection policy should map to a specific business risk, whether financial exposure, legal liability, or community safety. Second, the complete policy should be reviewed by legal counsel familiar with fair housing law in the jurisdictions where the firm operates, and updated annually or when regulations change. Third, training should ensure that team members understand the rationale behind each criterion, reinforcing that the policy is built on risk analysis and applied without variation.

Tenant identification, at its core, is a discipline. The firms that treat it as one will build portfolios that perform more predictably, carry less institutional risk, and demonstrate the kind of operational rigor that owners and agencies increasingly expect.

About the Author

James M. Davis is the founder of Awarded, LLC, an RFP consulting firm that helps property management companies evaluate, pursue, and win competitive bids. Before launching Awarded, Davis spent 17 years in property management operations, holding roles from leasing agent to interim COO and Regional VP across Midwest and California-based firms.

{kind=link}